Microfinance is the practice of providing financial services - including loans, savings, and insurance - to people who live in extreme poverty and may not have access to traditional banking services. The aim is to stretch limited funds - helping as many people as possible - by focusing on the aid that will most likely help people help themselves.

The general practice of microfinance has received a great deal of positive attention (one example being the 2006 Nobel Peace Prize), and anecdotes about its transformative effects are common; but evaluating its general impact on poverty raises difficult questions on which relatively little information exists. This page presents our views regarding the logical, and empirical, case for microfinance as a humanitarian anti-poverty measure.

Summary

How microfinance helps people: Anecdotes are common about using loans to expand personal businesses, but we are skeptical that these anecdotes are broadly representative. However, we believe that microfinance may often benefit people by helping them smooth consumption, manage their lives, and plan for uncertainty.

When microfinance helps people: We believe that nonprofit microfinance is likely to be a strong humanitarian intervention for people who have low and unstable incomes; would not otherwise have access to financial services; and use any loans sustainably, such that they are able to repay them.

What the empirical evidence says: Most studies of microfinance's impact have serious methodological limitations, but the strongest studies we've seen generally indicate that microfinance programs - when meeting the conditions above - have improved clients' standards of living.

Conclusion: We would guess that microfinance is generally a strong and cost-effective humanitarian intervention, where it serves low-income people who would not otherwise have access to financial services, and are willing and able to repay any loans they take out. However, existing empirical information about this intervention is very far from what it would need to be to give us high confidence.

The details

Table of Contents

How microfinance helps people

From what we've seen, anecdotes about microfinance programs generally focus on clients who use loans to expand personal ventures, and it is often implied that each loan leads to a permanent increase in income. Both of our finalists in this area provide such anecdotes: for example, the Grameen Foundation tells of a woman who used loans to purchase new materials and expand her textile business, and Opportunity International tells of a woman who used a loan to start a leather-making business.

Are these stories broadly representative of how most or all loans are used in such programs? From the little data we've seen (summarized below), we believe there is good reason to be skeptical of this idea, and to believe that the loans made through microfinance programs are often used for food, clothing, and other "consumption" activities.

However, we believe that microfinance can help people manage financial risk and volatility - and therefore improve their lives - even if it is not literally helping them to expand businesses. And for someone with extremely low income, being equipped to deal with volatility could make a substantial difference in standard of living. Two examples:

- Several researchers studying a microfinance program in Bangladesh agreed that "microfinance leads to consumption smoothing (consumption that is less variable over time) ... household consumption increased most during the lean Aus season, when the poor often go hungry."1

- "The economic lives of the poor," a survey-based study of people in extreme poverty around the world, notes that health problems are the most frequently cited source of stress2 , and that those who become ill pay for care by taking children out of school, borrowing directly, selling land, or choosing to forgo treatment.3

Relatively little empirical evidence exists on how loans from microfinance programs are actually used, but what we have seen makes us believe that there is generally a mix of the uses cited above: loans are sometimes used for business expansion, and sometimes used to manage risk and volatility as in the examples above.

- An evaluation of 500 clients in a rural development program in Bangladesh found that 80% of the average loan went to "productive investments" such as livestock, petty trade, land purchases, etc.4 . Of the remaining 20%, about half went to consumption and half went to paying off existing loans and mortgages 5 . In addition, just over 45% of clients studied used loans to cope with income variations caused by personal crises and crop losses.6

- An impact assessment in Mali7 found that 67% of second-year clients and 39% of first-year clients used loans partially to purchase clothing and other goods for their families, and that 7% of second-year clients and 18% of first-year clients used funds to purchase food8 .

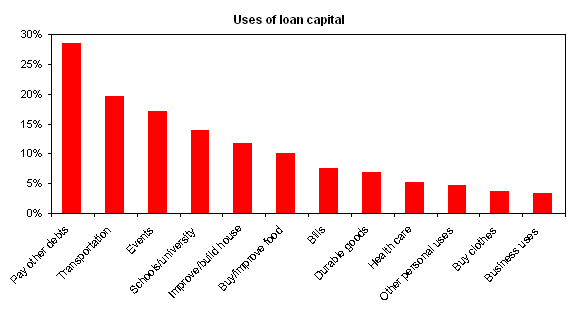

- "Expanding Credit Access: Using Randomized Supply Decisions to Estimate the Impacts" by Karlan and Zinman (2007), studied the effects of a lending program in South Africa, and provides a detailed breakdown of how loans in that program were used9 . (Note that the total is greater than 100% because respondents could state more than one use of the loan proceeds.)

{kind=link}

When microfinance helps people

As explained above, the specifics of how a microfinance program helps its clients can be highly varied, and it isn't necessarily true that only those with business expansion opportunities can benefit. Rather than try to list all the situations in which microfinance might improve people's lives, we find it appropriate to generalize that it will provide substantial benefits to people who:

- Face considerable economic uncertainty, such that the ability to manage financial risk and "smooth consumption" is important to their standard of living.

- Do not already have access to financial services, making microfinance programs (which are generally highly subsidized) necessary.

- Are willing and able to "pay" a fair price (i.e., premiums for insurance or interest on loans) for financial services. A person's willingness to take grant-based aid - or take out loans which they do not repay - is not itself a strong indicator that the aid is benefiting them (and a separate assessment of need is likely necessary to determine this). By contrast, the simple fact of a person's purchasing insurance or repaying a loan is likely a strong indicator that this service is providing a benefit.

It is relatively common for microfinance organizations to have data available on repayment rates for loans, a strong indicator of #3 (although not a perfect one - for example, Coleman (1999) noted one village in which two-thirds of clients "regularly borrowed from a moneylender to repay their village bank loans").10

#1 and #2 are much more difficult to assess; no organization we've spoken to has been able to provide data that is directly relevant to these considerations. The general study of poverty cited above gives some relevant information. It indicates that the very poor generally do face extreme financial volatility (as described above). It also indicates that many (30-70%) of the very poor have loans from non-traditional sources of credit (often family), although not from traditional sources.11

What the empirical evidence says

We have found many studies evaluating microfinance programs and pointing to improvements for clients (along such dimensions as income, spending, and in some cases broader quality-of-life measures). However, very few of these studies convincingly show that such improvements are attributable to the programs, as opposed to alternative explanations. (For example, many studies point to the superior well-being of participants compared to non-participants; but the mere fact that a person signs up for such a program could indicate a combination of motivation and existing economic opportunities, and such people may be positioned for increases in income with or without the program's help).

The studies that most convincingly "isolate" the effect of programs generally indicate that the microfinance programs have positive effects on people's lives. However,

- There are few such studies, and each is specific to a particular time and place.

- The positive effects found in these methodologically strong studies are generally smaller than the effects that would have been shown using simpler, more common methodology.

Therefore, we consider the evidence in favor of microfinance programs to be extremely limited, and while we find it encouraging, we do not believe it supports a blanket statement such as "microfinance has been shown to improve clients' lives in general."

Below, we summarize the strongest studies we know of that examine the effects of microfinance programs. We drew heavily on two literature reviews; Goldberg (2005) and, Karlan and Goldberg (2006), in finding and interpreting these studies.

Methodologically strong studies

Karlan and Zinman (2007) evaluated a consumer loan program in South Africa by starting with a group of people who had narrowly failed to qualify for loans, and randomly suggesting that some of them be reconsidered by loan officers (about half of those reconsidered ended up receiving loans). By following both those who had been suggested for reconsideration and those who had not - and knowing that randomization had been used to separate the two groups - the researchers were able to make a compelling case that the differences between the two groups could be attributed to the effects of the loans themselves. They found that those who had been suggested for reconsideration (and who had thus been more likely to receive loans) were significantly better off 6-12 months later on measures of income, reported hunger, and employment status.12

Coleman (1999) evaluated a microfinance program in northern Thailand, studying program participants, non-participants, and what we call "willing non-participants": people who had signed up to participate in the program even though it was not yet available in their village. He found that microfinance clients were better off than those who chose not to participate, by a variety of metrics (including expenditures on health care and education). However, he found no positive effects (and some negative effects) for microfinance when comparing participants to "willing non-participants." We agree with his position that the latter comparison is more appropriate, because it is closer to isolating the effect of the program itself, as opposed to the differences between those who were and weren't interested in participating.

Coleman points out that both participants and non-participants likely already had access to credit, through Thailand's state-run Bank for Agriculture and Agricultural Cooperatives.13 Therefore, his result is not necessarily a major strike against the effectiveness of microfinance programs in general. However, we find his result important for two reasons:

- It reinforces the idea (which we argue above) that microfinance is unlikely to do much good in areas with strong alternative sources of credit.

- It shows that simpler studies, which fail to capture the effects of clients' choice to enter or abstain from a program, can exaggerate the effects of a microfinance program (since those who choose to participate may have advantages unrelated to the actual effects of the program). We discuss these issues more below.

Alexander (2001) studied an urban microfinance program in Mibanco, Peru, using a similar approach to Coleman's (1999). Where Coleman (1999) compared program participants to "willing non-participants" (people who could not participate because the program was not available in their village), Alexander compared participants to "future participants": people who would later (according to available data) participate in microfinance programs, but were not yet doing so. Like Coleman (1999), she found that the choice to participate in a microfinance program is important, and that simply comparing clients to non-clients would therefore overstate the impact of the program. However, unlike Coleman (1999), she found that this phenomenon could not explain the entire difference between program participants and non-participants, and concluded that the microfinance program had positive effects on income.

We are not highly confident in this finding. As shown on Pg 13, participants and "future participants" differed in many other ways, and we would guess in general that "future participants" are not nearly as similar to actual participants (in terms of their current motivation, optimism, opportunities, etc.) as the "willing participants" Coleman (1999) studied (whose only reason for not participating in the program was that it was unavailable to them). Comparing participants to "future participants" potentially has some of the same drawbacks as comparing new clients to mature clients (these issues are discussed further below). However, Alexander's paper is among the strongest attempts we've seen to deal with the potential biases of microfinance studies (discussed more below), and we believe it represents suggestive evidence for the potential of microfinance programs to improve lives (though not nearly as strong evidence as Karlan and Zinman 2007, cited above).

Khandker (1998), Pitt, et al. (2003), and Khandker (2005) all examined a microfinance program in Bangladesh using a rich data set and a highly complex set of methods. These methods aimed to compare program participants to people who would likely have participated (according to a variety of statistical models) but were ineligible (due to a variety of sub-program restrictions based on village, gender, and owned land). All three analyses concluded that the microfinance program had a significant positive effect on participants' consumption, and the later studies also pointed to village-wide increases in consumption for those villages in which microfinance was available.

These studies rely heavily on statistical extrapolation about who would likely have participated in programs, and they are far from the strength and rigor of the Karlan and Zinman (2007) study listed above, but they provide somewhat encouraging support for the idea that the program studied had a widespread positive effect.

Other studies

A variety of other studies are referenced in Goldberg (2005) and Karlan and Goldberg (2006), but we do not believe that these studies (or any other studies we've encountered) provide compelling evidence for or against the programs they examined.

Some studies of microfinance programs simply track income, consumption, etc. for clients; we feel that the changes observed in such studies have too many possible explanations outside the programs themselves (including village-level economic changes) to serve as compelling evidence about programs' effectiveness.

Other studies compare microfinance clients to “comparison groups” of non-participants, in the hopes that any differences (in income, consumption, standard of living, etc.) can be attributed to the programs themselves. We find these studies problematic for a variety of reasons, which we outline below. (Note that the overviews by Karlan and Goldberg generally acknowledge that the studies discussed are prone to the methodological issues we discuss below.)

Possible problems with studies comparing clients to non-clients

Many studies compare microfinance clients to "comparable" non-clients, in order to get a sense of the difference the program makes. Sometimes such "comparability" is determined simply on the basis of geographical location, while some studies seek to compare clients to non-clients of similar age, education, etc. However, any study with this basic approach may be subject to:

- Qualification bias: the difference between clients and non-clients can be a function of the microfinance program's own criteria - meaning that those who are accepted into a program (the "client" group) may be more capable to begin with than those who are not.

- Participation bias: the less "qualification bias" there is - the more it can be said that clients and non-clients are equally qualified to join a program - the more the difference between them can be attributed to choice. It may be that those who choose to participate have characteristics such as optimism, motivation, and existing opportunities that lead to higher incomes regardless of the impact of the program itself.

- Location bias: many studies make comparisons between one geographical area (one where microfinance programming is offered) and another (where it is not). These studies raise questions about how comparable the two areas were to begin with.

Possible problems with studies comparing new clients to mature clients

Some studies attempt to control for the above biases by comparing new clients and pre-existing (mature) clients (rather than clients and non-clients). This method may mitigate the three concerns above: all people being studied have qualified to participate, have chosen to participate, and are in the same geographical location, but some of them have already participated in the program whereas others have yet to participate. Therefore, differences between the two groups may point to the impact of participation itself, rather than pre-existing differences in the groups being compared.

However, this method depends on comparing people who have joined a program at different points in time, and it is thus subject to the following three forms of bias:

- Survivor bias: mature clients may represent only those clients who are financially successful enough to continue "paying" for financial services (in particular, repaying loans with interest), while new clients may include future dropouts.

- "Wait-and-see" bias: some clients may choose to join a microfinance program only after it has established a track record, while others may be willing to sign up immediately; comparing new and mature clients may implicitly be comparing these two different types of people. While it's unclear exactly how these clients differ from clients who joined the program when it began, it seems likely that they are indeed different in important ways such as their degree of risk aversion or the age of their enterprises.

- Bias caused by changes in program characteristics: Individual microfinance institutions may change their location, targeting of types of clients, or evaluation of potential borrowers. These changes could lead to the qualification and location biases mentioned above even in a comparison of clients of the same microfinance institution.

Alexander-Tedeschi and Karlan (2006) give more detail on these forms of bias and provide an empirical example of the perils of comparing new to mature clients. Unlike most studies, which simply compare new and mature clients at the time of the study, Alexander-Tedeschi and Karlan (2006) tracked clients over time so that a comparison could be made between new clients and mature clients at the time they entered the program. They found that mature clients had been significantly better off than new clients (as measured by total household income, expenditures on household appliances, and expenditures on children's education) at the time of their first loan. 14

Conclusion

We believe that significantly more study is needed to have strong confidence in microfinance programs in general; however, the same applies to the other poverty-fighting programs we've evaluated.

Knowing what we know, we would bet that a microfinance program is significantly improving people's lives when it serves poor people with little access to credit, and when these people demonstrate a willingness and ability to “pay” for financial services. Moreover, such programs focus on enabling clients to solve their own problems rather than prescribing pre-determined solutions for them, and are likely to be highly cost-effective (making the most of each dollar by asking clients to repay loans and otherwise contribute whatever they can). Therefore, we feel slightly more confident in microfinance programs than in the other economic assistance programs we've examined, which generally have less empirical evidence behind them than even the few studies we've cited here.

Sources

Papers specifically referred to above

- Alexander, Gwendolyn. 2001. An empirical analysis of microfinance: Who are the clients? (DOC). Working Paper. Northeast Universities Development Consortium (NEUDC).

- Alexander-Tedeschi, Gwendolyn and Dean Karlan. 2006. Cross sectional impact analysis: Bias from dropouts (PDF). Working Paper.

- Banerjee, Abhijit V. and Esther Duflo. 2006. The economic lives of the poor (PDF). Department of Economics Working Paper 06-29. Cambridge: MIT.

- Coleman, Brett E. 1999. The impact of group lending in Northeast Thailand (PDF). Journal of Development Economics 60:105-141.

- Goldberg, Nathanael. 2005. Measuring the impact of microfinance: Taking stock of what we know (PDF). Washington, DC: Grameen Foundation USA Publication Series.

- Husain, A. M. Muazzam. 1998. Poverty alleviation and empowerment: The second impact assessment study of BRAC's rural development programme (PDF). Dhaka: BRAC.

- Karlan, Dean and Jonathan Zinman. 2007. Expanding credit access: Using randomized supply decisions to estimate the impacts (PDF). Economic Growth Center Discussion Paper 956. New Haven: Yale University.

- Karlan, Dean and Nathanael Goldberg. 2006. The impact of microfinance: A review of methodological issues (PDF). Working Paper. New Haven: Innovations for Poverty Action.

- Khandker, Shahidur. 1998. Fighting Poverty with Microcredit. Dhaka: University Press Limited.

- Khandker, Shahidur. 2005. Microfinance and poverty: Evidence using panel data from Bangladesh. World Bank Economic Review 19 (2): 263-286. Abstract available at http://wber.oxfordjournals.org/content/19/2/263.abstract (accessed November 28, 2010). Archived by WebCite® at http://www.webcitation.org/5uaxvZczf.

- MkNelly, Barbara and Karen Lippold. 1998. Practitioner-led impact assessment: A test in Mali (PDF). Washington, DC: AIMS.

- Pitt, Mark, et al. 2003. Credit programs for the poor and the health status of children in rural Bangladesh. International Economic Review 44(1): 87-118. Abstract available at http://ssrn.com/abstract=377084 (accessed November 28, 2009). Archived by WebCite® at http://www.webcitation.org/5uazhywRE.

Additional relevant studies

- Barnes, Carolyn. 2001. Microfinance program clients and impact: An assessment of Zambuko Trust, Zimbabwe (PDF). Washington, DC: AIMS. Impact study. Compares clients to non-clients.

- Barnes, Carolyn, Gary Gaile, and Richard Kibombo. 2001. Impact of three microfinance programs in Uganda (PDF). Washington, DC: AIMS. Impact study. Compares clients to non-clients.

- Brüntrup, Michael, et al. 1997. Impact assessment of ASA. Dhaka: The Association for Social Advancement. Impact study. Compares clients to non-clients and new clients to mature clients.

- Chen, Martha A. and Donald Snodgrass. 2001. Managing resources, activities, and risk in urban India: The impact of SEWA Bank (PDF). Washington, DC: AIMS. Impact study. Compares clients to non-clients.

- Dunn, Elizabeth. 2005. Impacts of microcredit on clients in Bosnia and Herzegovina. Foundation for Sustainable Development of the Federation of Bosnia and Herzegvonia and Republika Srpska Development and Employment Foundation. Impact study. Compares clients to non-clients.

- Dunn, Elizabeth, and J. Gordan Arbuckle, Jr. 2001. The impacts of microcredit: A case study from Peru (PDF). Washington, DC: AIMS. Impact study. Compares clients to non-clients.

- Edgcomb, Elaine L. and Carter Garber. 1998. Practitioner-led impact assessment: A test in Honduras (PDF). Washington, DC: AIMS. Impact study. Compares new clients to mature clients.

- Faisel, Arjumand. 2004. Impact assessment of Kashf's microfinance and Karvaan enterprise development programme. Islamabad: Arjumand and Associates. Impact study. Compares clients to non-clients.

- Gibbons, David, ed. 2005. Moris Rasik: An interim impact assessment. Manuscript. Impact study. Compares new clients to mature clients.

- Hishigsuren, Gaamaa, Brian Beard, and Lydia Opoku. 2004. Client impact monitoring finding from Sinapi Aba Trust, Ghana. Oak Brook, IL: Opportunity International. Impact study. Compares new clients to mature clients.

- Hossain, Mahabub. 1988. Credit for the alleviation of rural poverty: The Grameen Bank in Bangladesh (PDF). Research Report 65. Washington, DC: International Food Policy Research Institute. Impact study. Compares clients to non-clients.

- Hossain, Mahabub and Catalina P. Diaz. 1997. Reaching the poor with effective microcredit: Evaluation of a Grameen Bank replication in the Philippines (PDF). Los Baños: International Rice Research Institute. Impact study. Compares new clients to mature clients.

- MkNelly, Barbara and Christopher Dunford. 1998. Impact of credit with education on mothers and their young children's nutrition: Lower Pra Rural Bank credit with education program in Ghana. Davis, CA: Freedom from Hunger. Impact study. Compares clients to non-clients.

- MkNelly, Barbara and Christopher Dunford. 1999. Impact of credit with education on mothers and their young children's nutrition: CRECER credit with education program in Bolivia. Davis, CA: Freedom from Hunger. Impact study. Compares clients to non-clients.

- Neponen, Helzi. 2003. ASA-GV microfinance impact report 2003. Trihcirappalli: The Activists for Social Alternatives. Impact study. Compares new clients to mature clients.

- Todd, Helen. 2000. Poverty reduced through microfinance: The impact of ASHI in the Philippines (PDF). Washington, DC: AIMS. Impact study. Compares clients to non-clients.

- Todd, Helen. 2001. Paths out of poverty: The impact of SHARE Microfin Limited in Andhra Pradesh, India. Unpublished Report. Brighton, UK: Imp-Act. Impact study. Compares new clients to mature clients.

- Tsilikounas, Caroline. 2000. ICMC and Project Enterprise Bosnia and Herzegovina (PDF). Washington, DC: AIMS. Impact study. Compares new clients to mature clients.

- 1

Goldberg 2005, Pg 19.

- 2

Banerjee and Duflo 2006, Pg 9.

- 3

Banerjee and Duflo 2006, Pg 16.

- 4

Husain 1998, Pgs 62-63.

- 5

Husain 1998, Pg 63.

- 6

Husain 1998, Pg 105.

- 7

MkNelly and Lippold 1998.

- 8

Husain 1998, Pg 28.

- 9

Karlan and Zinman 2007, Pg 41.

- 10

Coleman 1999, Pg 108.

- 11

Banerjee and Duflo 2006, Pg 37.

- 12

Karlan and Zinman 2007, Pgs 20-21.

- 13

Coleman 1999, Pg 119.

- 14

Alexander-Tedeschi and Karlan 2006, Pg 15.